In this article, we take a look at the agriculture sector in India and how technological interventions by the agritech sector are creating investment opportunities by raising efficiencies and overall productivity. Private equity investments into agritech (INR 66 billion) grew more than 50 percent annually over four years till 2020. Overall, the agritech ecosystem has attracted a surge of startups in India offering technology-based solutions like offtake marketplaces, storage and transportation services, and agronomy advisory services while large traditional players seek to reduce operational costs and manage scale more efficiently. India's Budget 2022-23 also contains provisions to support 'digital agriculture'.

As the global population reaches 7.9 billion in November, and estimated to reach 9.8 billion by 2050, food security has become a top concern across the world. The urgency for action also needs to address the scarcity of resources, distortions in distribution and access, and the need to expand agriculture outputs. Policymakers everywhere are now seeking sustainable methods to leverage technology in agricultural practices to alleviate this crisis.

It has catapulted the attention given to emerging agriculture technology (agritech), with startups in the area raising US$26.1 billion in funds in 2020 worldwide. This was a 35.4 percent growth over 2019. In fact, the global agritech market is projected to grow at a compound annual growth rate (CAGR) of 12.1 percent between 2020-27. India, too, is competing in this segment alongside China and the US.

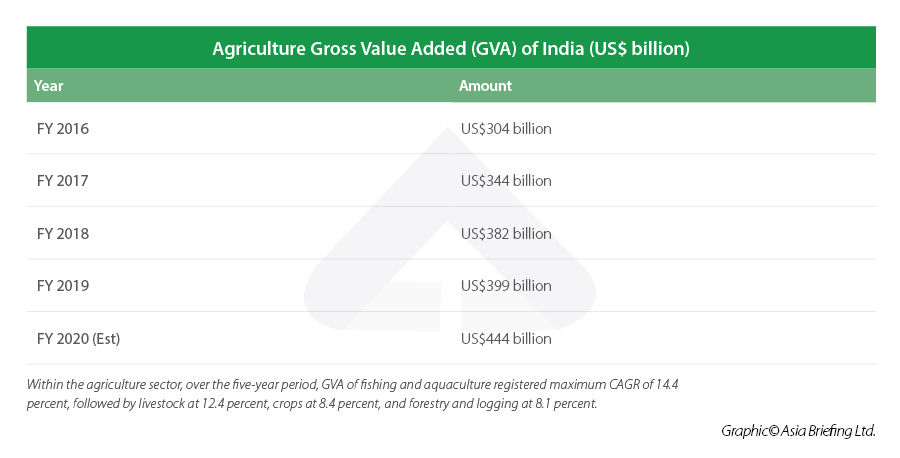

Developments in agritech are hugely relevant to India’s economy. Its agriculture sector, which is worth US$370 billion, continues to remain the main source of livelihood for over 40 percent of the population and contributes 19.9 percent (FY 2021) to the national GDP. However, despite the sector's contribution, it remains mired in structural weakness that inhibit growth and productivity. In order to address these challenges and improve farmer’s incomes, Indian agriculture needs technology-aided modernization, backed by resilient reforms - this is where agritech is expected to play a significant role.

India currently has over 1300 agriculture startups - which are actively employing artificial intelligence (AI), machine learning (ML), internet of things (IoT), etc. - to increase efficiency and productivity in the sector. The COVID pandemic has now put them on an upwards growth trajectory. The states of Karnataka and Maharashtra and the Delhi National Capital Region (NCR) are major hubs for agri-startups in India.

In this article, we take a look at India's agriculture sector and how interventions by agritech players are creating investment opportunities by raising efficiencies and overall productivity.

Contribution of the agriculture sector to India's economy

Indian agricultural sector broadly comprises of farming (crops and horticulture) and forestry, livestock (milk, eggs, meat), and fisheries. Ranking second after China, it accounts for 11.9 percent of the global agriculture gross value added (GVA) of US$3,320.4 billion and contributes 12 percent to India’s exports. Additionally, the sector also impacts consumption and production dynamics in non-agricultural segments, such as consumer products, retail, chemicals, and e-commerce.

The economic interlinkages make the agricultural sector central to India's economic output and growth potential. It's also why reforms in the sector are sorely needed. We breakdown long time challenges below.

Fragmented and unorganized agribusiness ecosystem in India

The agribusiness ecosystem comprises the business activities undertaken from farm to fork, covering the entire value chain, from the supply of agricultural inputs, the production and transformation of agricultural products, and their distribution to final consumers. This ecosystem has further expanded to segments, such as e-commerce and hyperlocal, propelled by factors like swift urbanization, diet diversification, evolving consumer preferences, and expansion of food markets.

However, it remains largely unorganized and fragmented, with existence of multiple levels of intermediaries and middlemen across the agriculture value chain. While 86 percent of the small and marginal farmers remain the primary providers of food and nutrition to India, they remain constrained by issues like extremely small landholdings of less than two hectares and limited access to technology, inputs, credit, capital, and market etc.

Agritech innovation can plug these challenges, such as lack of infrastructure, supply chain inefficiencies, and low digital adoption - which have historically held back the sector from performing to its full potential.

How agritech aids productivity and efficiency in India's agriculture sector

Agritech primarily refers to an ecosystem of companies and startup enterprises that are capitalizing on technological advancements to deliver products or services for increasing yield, efficiency - both in terms of time and cost, and profitability for farmers across the agriculture value chain. The various segments within the agritech sector, which support the overall value chain are:

- Market linkage – farm inputs: Digital marketplace and physical infrastructure to link farmers to inputs.

- Biotech: Research on plant and animal life sciences and genomics.

- Farming as a service: Farm equipment for rent on a pay-per-use basis.

- Precision agriculture and farm management: Use of geospatial or weather data, IOT, sensors, robotics etc. to improve productivity; farm management solutions for resource and field management, etc.

- Farm mechanization and automation: Industrial automation using machinery, tools and robots in seeding, material handling, harvesting, etc.

- Farm infrastructure: Farming technologies, such as greenhouse systems, indoor-outdoor farming, drip irrigation, and environmental control, such as heating and ventilation, etc.

- Quality management and traceability: Post-harvest produce handling, quality check and analysis, produce monitoring, and traceability in storage and transportation.

- Supply chain tech and output market linkage: Digital platform and physical infrastructure to handle post-harvest supply chain and connect farm output with the customers.

- Financial services: Credit facilities for input procurement, equipment, etc. as well as insurance or reinsurance of crop.

- Advisory/ Content: Information platforms online platform for agronomic, pricing, market information.

Agritech provides opportunity to plug several pain points that exist in the agriculture sector at present across the value chain, thereby expanding the market potential. Leveraging technology in India's agriculture sector can create opportunities for investment through modernizing and introducing systemic efficiencies.

Some ways in which this can be achieved are:

- Facilitating input market linkages supported with robust physical infrastructure network can address the existing issues related to volatility in input prices as well sub-optimal input selection.

- Precision agriculture can enhance yield by up to 30 percent.

- Digitalizing records through farm management can improve operational efficiencies and save costs.

- Introducing quality management and traceability will help farmers attain better outcomes in terms of high quality produce, further incentivizing them to continue with modern methods.

- Facilitating output market linkages through efficient post-harvest supply chain by eliminating inefficiencies, such as high wastage of farm produce, which is a win-win for both farmers as well as consumers.

- Offering better financial services, which could serve 30 percent of farmer households through access to credit, and 65 percent of farmer households through access to crop.

Business models in India's agritech sector

The business models within the agritech space be classified into:

- Margin-based model: Segments such as market linkage – farm inputs, supply chain technology, and output market linkage operate through this model where the agritech player earns a margin by creating marketplace linkages at the input or output side, and by executing the promised services.

- Subscription-based model: Agritech players operating in segments like precision agriculture and farm management as well as quality management and traceability offer a mix of hardware, software, and services-based solutions throughout the year and collect monthly or annual subscription charges from their customers.

- Transaction-based model: Agritech companies dealing in the financial services segment follow this model based on the number of loans or insurance policies served.

Overview of agritech in India

The overall agritech ecosystem witnessed a revenue growth of approximately 85 percent during FY 2019-20. An Ernst & Young 2020 study pegs the Indian agritech market potential at US$24 billion by 2025, of which only one percent has been captured so far. A study by Bain & Company pegs this potential at US$35 billion by 2025.

Meanwhile, another Bain & Company report, jointly produced with the Confederation of Indian Industry (CII) in March 2022, indicates that private equity investors have focused on systemic issues in the agritech industry and its sustainable development. Private equity investments in agritech startups between 2017 and 2020 amounted to INR 66 billion, growing at the rate of over 50 percent. Supporting this has been the growth of the rural microfinance sector - from INR 1.22 trillion in December 2019 to INR 1.46 trillion in March 2021. Agri credit grew from INR 8 trillion in FY 2014-15 to INR 14 trillion in FY 2019-20.

The Bain-CII report notes that a surge of agritech startups have entered the ecosystem to offer technology-based solutions like offtake marketplaces, storage and transportation services, and agronomy advisory services while large traditional players seek to reduce operational costs and manage scale via in-house solutions and new partnerships with emerging players. Global technology giants, like IBM and Microsoft, are looking at innovative solutions for crop health monitoring and yield estimates, for example.

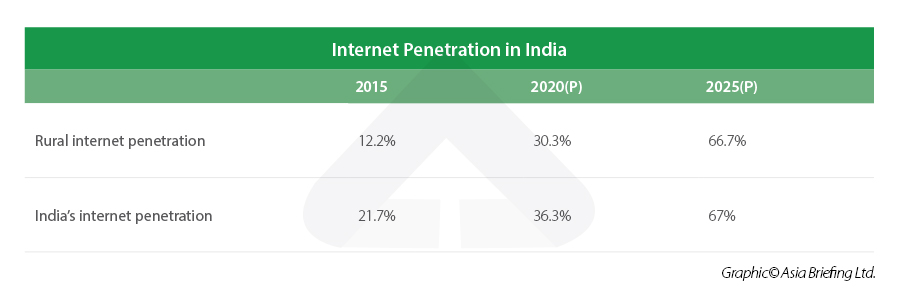

With ever increasing internet penetration in the country, and rural regions being the primary driver of this growth, India stands well equipped to adapt to changing methodologies in agriculture and transition from conventional business models to various innovative business models propelled by agritech.

Budget 2022-23 provisions

When presenting this year's budget, Finance Minister Nirmala Sitharaman announced that a new scheme will be developed in partnership with the private sector to deliver digital and hi-tech services to farmers. This will integrate public sector research with private agritech players within the agricultural value chain. In her Budget 2022-23 speech, Sitharaman said that INR 600 million will be allocated for 'digital agriculture'.

The government hopes to launch a fund with blended capital to finance startups for agriculture and rural enterprises that focus on the farm-produce value chain. The finance minister also mentioned the use of drone-based technologies to benefit agriculture, such as in crop assessment, digitization of land records, and spraying insecticides and nutrients.

Investing in India's agritech space

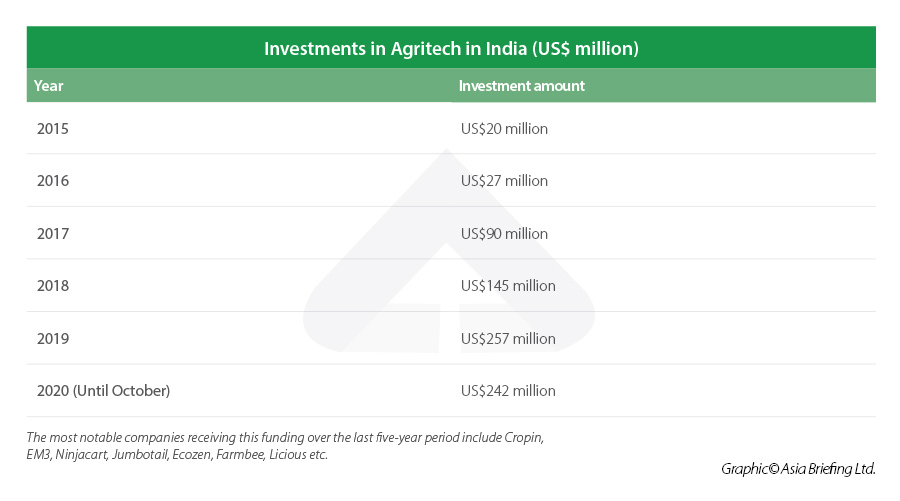

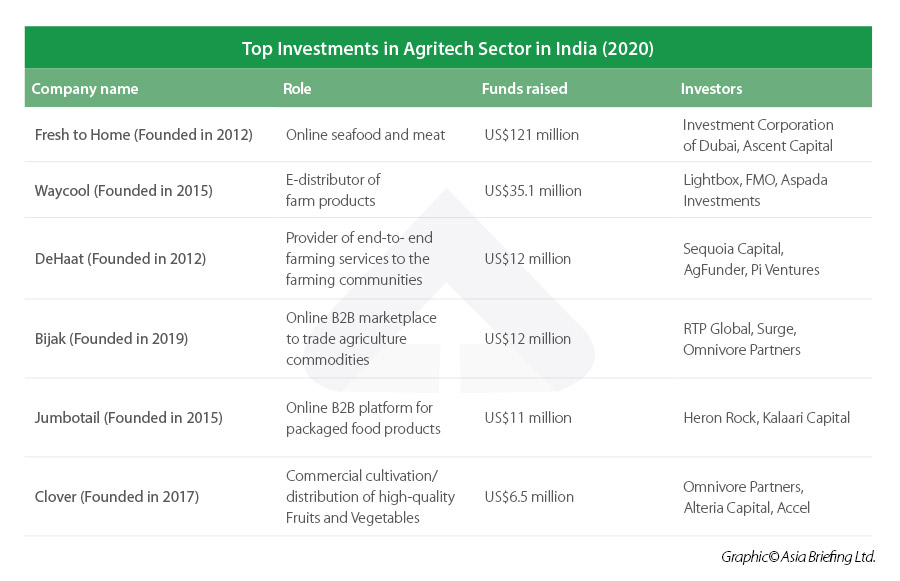

The table below depicts the steady rise of investments in the Indian agritech landscpe with most prominent companies receiving funding being EM3, Cropin, Jumbotail, Ninjacart, DeHaat, AgroStar, Farmbee, Licious, and Zappfresh.

Since 2015, the investments in Indian agritech have expanded multifold with total investment in 2020 (until October) being US$242 million. In 2020, within the agritech industry, the meat delivery segment of startups received the maximum funding of US$124 million, followed by startups engaged in marketplace and e-distribution (US$83 million).

The 2020 figures are a major deviation from the 2019 trends where marketplace and e-distribution startups received the lion’s share of funding at US$203 million out of the total US$257 million received, while the meat delivery startups received merely US$20 million in funding.

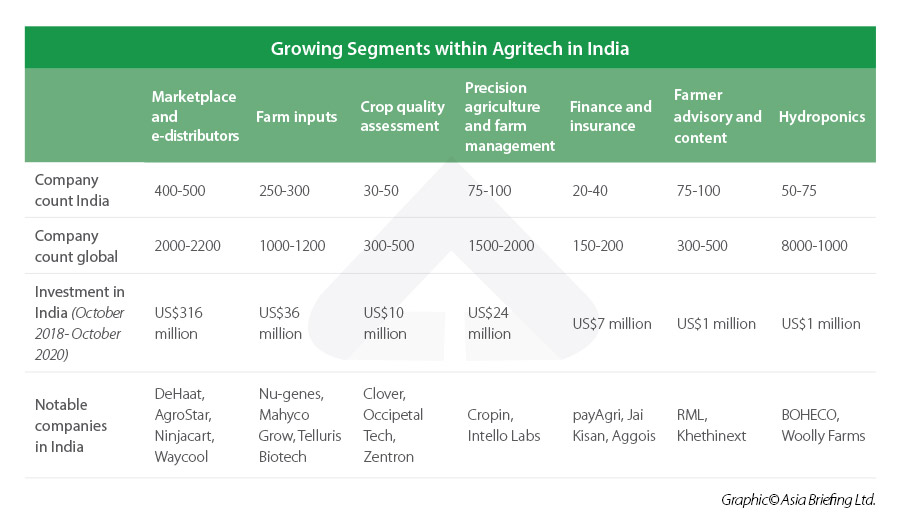

Growing segments within agritech in India

Out of the total projected agritech market potential of US$24 billion, the supply chain technology and output markets segments have the highest potential in India, worth US$12.1 billion, followed by financial services (US$4.1 billion), precision agriculture and farm management (US$3.4 billion), quality management and traceability (US$3.0 billion), and market linkages-farm inputs (US$1.5 billion).

Some of the most prominent companies involved in different agritech segments include:

- IoT powered agriculture and drones: Fasa, Bitmantis, Agronxt, Soilsens

- Marketplace and e-distributor: DeHaat, Ninjacart, Jumbotail, Bijak, Farmzen

- Farm inputs: DeHaat, AgriBegri, AgroStar, BigHaat, Gramophone

- Precision agriculture and farm management: Cropin, FarmERP, AgNext, BharatAgri

- Farmer advisory: AgroStar, IFFCO Kisan, RML, Farmbee, Fasal Salah

- Finance and insurance: Aggois, Niruthi, Weather Risk, Jai Kisan

- Equipment leasing: EM3, Agri Bolo, Tractor Bazaar

- Meat delivery: Licious, Zappfresh, Pesca Fresh, Fresh to Home

- Crop quality assessment: Nebulaa, AgricX, Intello Labs

- Smart farm equipment: Drip Tech, Netafim, Cultyvate, Soilsens

- Hybrid seeds: Mahyco, Nu-genes, Nuziveedu seeds

- Hydroponics: Fresco, Triton Foodworks, Junga Fresh and Green, Absolute Foods

Input market linkage and farming as a service (FaaS) segment

This segment is fast picking up pace in India with prominent players being AgroStar and BigHaat, which offer missed call-based service for farmers ordering inputs and equipments along with cash-on-delivery service. These players have been able to eliminate multiple levels of intermediaries by partnering directly with the producers. Some companies also offer services, such as on-demand machinery rental, field levelling, and pesticide spraying, as a part of farming-as-a-service.

Supply chain, post-harvest management, and output market linkage segment

This segment is the largest contributor to the revenue of the agritech industry in FY 2020 and also witnessed maximum growth among all the segments during the same period. Players in the segment are involved in collection, processing, storage, and logistics and distribution of agriculture produce from farmers to end customers or retailers. Inadequate rural infrastructure and lack of traceability along the supply chain has prompted the intervention of agritech players in the segment. Startups including Ninjacart, Waycool, Samunnati etc. are engaged in this segment.

Precision farming, analytics, and advisory segment

This segment offering precision farming solutions and advisory services witnessed a growth of approximately 17 percent during FY 2020. The startups in this segment address structural issues arising out of lack of knowledge about scientific farming methods and techniques among famers. These players collect farm specific data about soil, weather conditions, humidity, pests etc. using IoT sensors or geospatial technology and use their analytical capabilities to provide timely insights to the farmers. Agritech startups are also coming up with quality assessment and grading solutions for large agribusinesses and traders. At present, there are approximately 200-250 startups in India dealing in these services. Prominent startups include Clover, Cropin, KhetiNext, Zentron, etc.

Agri fintech

This segment comprises of agritech startups offering solutions, such as credit, insurance, warehouse receipt financing, trade financing, etc. Inadequate access to organized credit, collateral, and formal documentation is the biggest challenge faced by farmers. Agritech players are leveraging technologies, such as geo tagging of farm lands and remote crop monitoring, to build risk profiles of farmers and ascertain their credit worthiness. By partnering with banks, NBFCs, and input suppliers, agritech players offer loans at lesser interest rates than unorganized lenders. This segment is still developing in India and has around 20-40 startups at present, with prominent players being payAgri, Jai Kisan, Aggois, etc.

This article was originally published in November 2021. It was last updated March 3, 2022.