- Step-by-step guide on starting an online business in India and e-commerce trends and emerging business models.

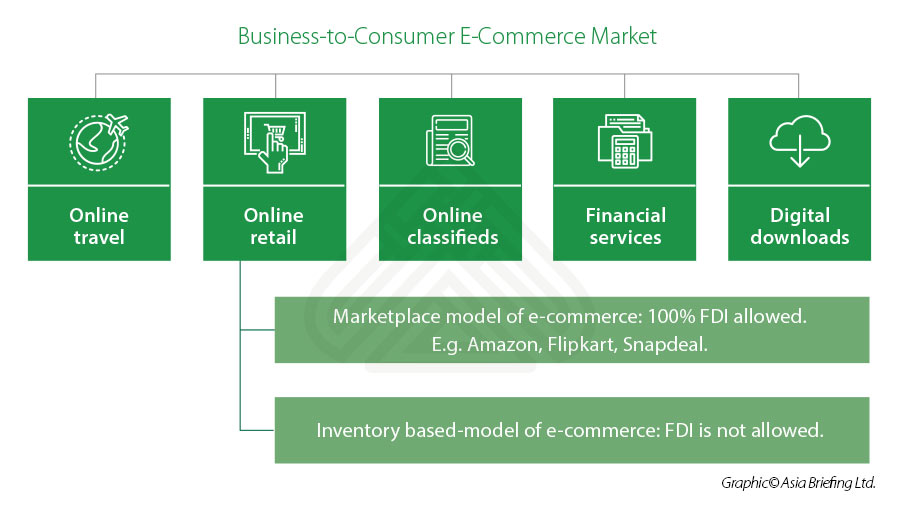

- 100% foreign direct investment (FDI) allowed under automatic route in B2B e-commerce and in marketplace model of e-commerce.

- 100% FDI allowed under government approval route for e-commerce by food retail companies if the products retailed are manufactured and/or produced in India.

[promote-webinar url="https://www.dezshira.com/events/details/expanding-your-business-in-india-s-ecommerce-sector-strategies-trends-and-compliance-insights-10076.html"]

Spurred by increasing smartphone penetration, an expanding internet user base, and rising consumer wealth, e-commerce platforms have revolutionized the way business is done in India. Estimated to be currently at 25 percent of the total organized retail market, India’s online retail segment is projected to reach a 37 percent share by 2030.

The country’s online market appeal is significant: it has a large domestic market base, rapidly growing Tier 2 and Tier 3 cities, a relatively young and trend-conscious consumer base, rising disposable incomes, several digital payment platforms, improving last mile logistics enabled by hyperlocal start-ups, and since the lockdowns last year – an accelerated preference for online shopping in urban areas through increased integration of e-marketplaces like Amazon, Zomato, Myntra etc. with social media platforms like Facebook and Instagram. This behavior has also replicated on the growth on online business service segments like gaming and fitness.

Such growth trends and shifting consumer patterns create highly attractive opportunities for foreign companies that may have previously hesitated to enter the country’s traditional retail space.

How to sell online in India

Step-by-step guide on how to sell online in India

Discovering market niche

The first step is working out what product(s) are to be sold and market research for the same. Once the cost feasibility is ascertained, it is important to create a digital catalogue of the products to be sold, which includes product code, product name, description, category, selling price, discount (if any), brand, color, and other applicable attributes.

Choosing a business model

Build own e-commerce website

Setting up a proprietary e-commerce website is suitable if the seller has a unique product to sell. However, it is both expensive and time consuming and requires a long time to establish market presence. It requires the setting up of an online store, integrating a secure payment gateway, and building a logistics chain, among other tasks. It is suitable for sellers who are looking for a long-term setup and intend to focus on building their brand name.

Sell on an established marketplace

Selling on an already established marketplace like Amazon, Myntra, or Flipkart is the easiest and most convenient way to sell products online, where the seller need not focus on developing logistics, payment gateway, or delivery channels as they are catered to by the marketplace. Foreign merchants can join any of these marketplaces. The process requires registering the company, obtaining a tax number, and opening a bank account. The marketplace will take care of logistics and payments.

Sell on social media platforms

Social network platforms, short form video and image platforms, and chat-based like Facebook, Instagram, WhatsApp, Twitter etc. have gained popularity due to their increased outreach among the consumers. Besides they are now an inevitable part of the digital marketing strategy of e-commerce and offline retail players to enhance their presence and visibility among the consumer base.

Registering the business

There are three modes of registering the business.

-

- Sole proprietorship;

- Private or public limited company; and

- Limited liability partnership.

A private limited company is often considered the most suitable option for smaller companies as well as foreign companies owing to a relatively easier, less expensive, and less stringent registration process which requires few documents as compared to LLP, which has stricter FDI regulations.

Logistics

An established marketplace will take care of the logistics. However, if the business decides to launch their own e-commerce store, logistics demand more in terms of both time and cost; however, investment in efficient logistics will prove beneficial in terms of brand image over the long run. International logistics players, such as FedEx and UPS, operate in India. Other players like DTDC, Delhivery, Bluedart, DHL etc. have also established efficient supply chains across the country. With the aid of logistics technology and growth of hyperlocal start-ups like Swiggy Go, Dunzo etc., delivery options are getting better – even able to serve India’s interior regions, such as Tier 2 and Tier 3 cities and towns.

Payments

Along with setting up a payment gateway in case of setting up their own e-commerce site, it is important to cater to the Cash on Delivery (COD) option, which is highly popular among the Indian consumers. However, the COD option is expensive for the merchants who have to pay multiple fees along with the courier charges. But, with increased digitization, digital wallets and payment apps, such as Paytm and GooglePay, are gaining popularity.

Induced by the fear of surface contact during the pandemic, adoption of digital payments is becoming a necessity. COVID-19 has thus moved large sections of the cash dependent Indian population towards getting familiar with online payments – a transition that would have otherwise required considerable costs as well as time, considering the skepticism among the populace in dealing with money matters online.

E-commerce industry in India: Market size, trends, and key players

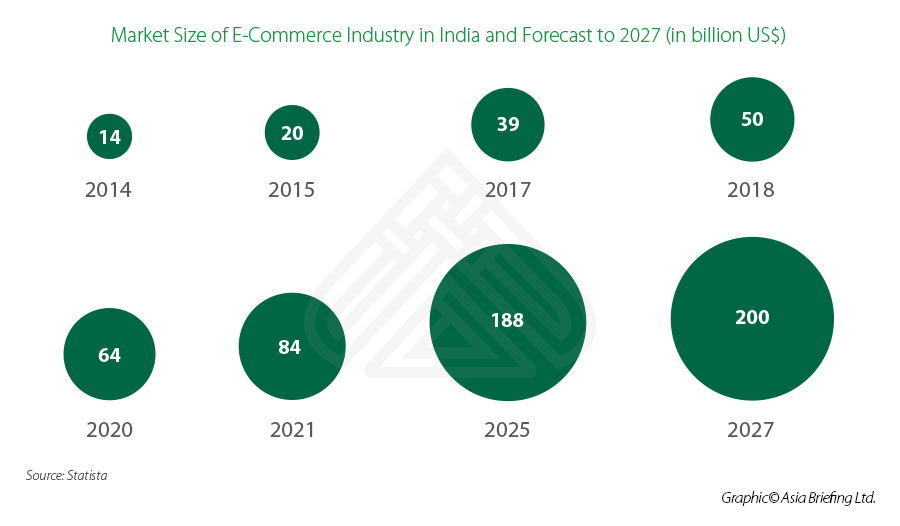

Led by e-commerce giants like Amazon India, Flipkart, Myntra etc., the Indian e-commerce market is riding high on the wave of Indian consumerism, that has picked up pace since 2005 due to favorable market conditions and policy support. India’s e-commerce market size was approximately US$50 billion in 2018 and is projected to reach US$200 billion by 2027.

Although the e-commerce industry experienced a temporary setback due to the pandemic (except for specific segments pertaining to daily consumption needs), the loss of momentum has quickly reversed its tracks. Post the COVID-19 related lockdowns and periodic night curfews, the online retail sector has witnessed an upsurge in the number of several first-time shoppers as well as increasing consumption by those familiar with online shopping. Many consumers, particularly in urban areas, appear to still be wary of frequently shopping in offline marketplaces due to heightened risk of infection.

However, a recent report by BCG-RAI report titled "Racing towards the next wave of Retail in India" expects a consumption led recovery for Indian economy, projecting its retail industry valuation at US$2 trillion by 2032. Within the retail industry, the e-commerce market is poised reach US$130 billion by 2026, as compared to US$45 billion in 2021. The report suggests that industry segments like food and grocery, restaurants and Quick service restaurant (QSR), consumer durables have already re-bounced post the Covid-19 disruption, other segments like jewellery and accessory, apparel, and footwear are also are driving this expansion in the consumption patters.

The upsurge of the post-COVID e-commerce industry is also confirmed by “The 2021 Global Payments Report” by the fintech firm Worldpay FIS. The report forecasts 84 percent growth for the global e-commerce sector, which could reach US$111 billion by 2024, propelled by mobile shopping.

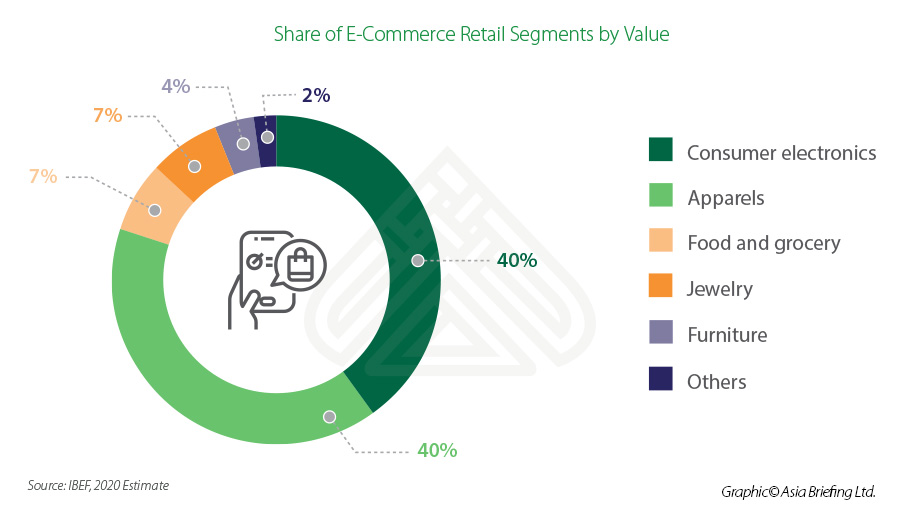

Data reveals that in the e-commerce retail market – consumer electronics, and apparels grab the majority share, with 40 percent each. The apparel fashion market is growing at a CAGR of 11 percent, within which the online fashion segment is growing the fastest at a CAGR of 32 percent. In the online apparels segment, e-marketplace platforms like Myntra, Jabong, Ajio, and Limeroad are leading the race by making fashion more affordable to the masses. Over the last year, major apparel and cosmetic giants like H&M, Uniqlo, Zara, Marks & Spencer, and MAC have also worked on increasing their online presence in India. H&M and MAC have adopted the dual strategy of selling on existing platforms like Myntra and Nykaa to boost short term sales as well launching their own e-commerce websites keeping long-term profitability and branding in mind.

Meanwhile, the Indian online food and grocery segment is heating up, fueled by fierce competition among start-up platform players like Flipkart, BigBasket, Zomato, and Swiggy as well as the entry of Amazon and traditional retail conglomerate Reliance JioMart.

Consumers are offered a range of products and deals in almost every segment, each platform seeking to capture loyal shoppers. The total size of the e-grocery market in the country was expected to grow from US$1.9 billion in 2019 to US$3 billion by 2020, according to a report by consultancy firm RedSeer and online grocery start-up, BigBasket. Several factors are driving this growth, most notably the decision to allow 100 percent FDI in the food retail market.

The lockdown has also ushered in changes and broadened the perceptions of kirana store owners (family-owned / mom-and-pop shops) across the country, who were previously skeptical of integrating with the e-commerce sector. The 12 million-strong network of kirana shop owners capture the lion’s share of India’s retail market and their integration with e-commerce platforms will ensure seamless delivery of merchandise along the length and breadth of the country. Flipkart has partnered with 27,000 kirana stores across 700 cities, while Amazon has partnered with 20,000 kirana stores. Reliance’s JioMart has also come forward to provide digital terminals to offline shopkeepers, for inventory management and stock ordering from Reliance’s network of wholesalers.

Drivers of e-commerce industry in India

Boasting a huge market size with a relatively young demography, India adds approximately 10 million daily active internet users each month. Rising population and disposable incomes in Tier 2 and Tier 3 cities along with the underserviced rural market promise immense potential in the sector. The smartphone penetration per 100 people has increased from 5.4 in 2014 to 26.2 in 2018. The number of internet connections in India increased from 560 million in 2018 to 760 million in 2020. The modernization of digital payments infrastructure, backed by BHIM/UPI and NEFT, has thrust India’s e-commerce growth by facilitating ease of pay. Start-up digital wallet players, like Paytm, PhonePe, MobiKwik, etc. also cater to the large unbanked population.

Other factors like postal reliability aiding in smooth delivery of services along with increased bank account penetration with aid of enabling initiatives like JAM trinity (Jan Dhan-Aadhar-Mobile) have also contributed to the impressive rise of the e-commerce industry.

Government policy support

- E-commerce draft policy: The Government of India’s Draft National E-Commerce Policy encourages FDI in the marketplace model of e-commerce. According to the draft, a registered entity is needed for the e-commerce sites and applications to operate in India.

- Bharat Net and Digital India: Under the Digital India movement, the Government has launched various initiatives like Unified Mobile Application for New-age Governance (UMANG), Bharat Interface for Money (BHIM) etc. to boost digitization. The BHIM served as a flagbearer in linking payments directly through banks, doing away with the need to transfer money to the mobile wallets first, as was earlier required by Paytm, PhonePe etc. Most of the private players have also followed suit to adopt the Unified Payment Interface (UPI) to make digital payments. Massive budgetary allocations in FY2021-22 amounting to US$95.33 million have also been made to further the objective of mass digitization in India.

- National Retail Policy: The government has proposed a National Retail Policy in which it acknowledged five key areas — ease of doing business, rationalization of the license process, digitization of retail, focus on reforms, and an open network for digital commerce. The proposed policy aims to integrate the administration of offline retail and e-commerce.

- Consumer Protection (E-Commerce) Rules 2020: These Rules direct e-commerce companies to display the country of origin alongside product listings. In addition, they will also have to reveal parameters like product image, product title, product description, product features, product ratings, and product review that will determine product listings on e-commerce platforms. Considering that the Indian market is still adapting to online shopping, these requirements will ensure the credibility of the seller and boost consumer confidence.

- E-commerce ecosystem: In order to provide easy access to all, including small traders and producers, the Department for Promotion of Industry and Internal Trade (DPIIT) set up a steering committee in November 2020 for formulation, implementation, and policy oversight of Open Network for Digital Commerce (ONDC). It will be a neutral platform that will work to set protocols for cataloguing, vendor discovery, and price discovery. Their aim is to provide equal opportunities to all marketplace players, including the consumers.

- 5G network: Substantial investments have been made by the Government of India in rolling out fibre network for 5G which will help boost Ecommerce in India.

The social commerce-based business model

Data suggests that online stores, which have a social media presence, registered 32 percent more sales on an average than the stores which do not have social media presence. Social media is thus among the most potent digital marketing tools – an intuitive insight given the amount of time we spend on our smartphones on average. More interestingly, these social media channels are also evolving into new e-marketplaces.

The outreach of social media has led to the development of a new segment, social commerce, an internet-based model for small and medium-sized businesses. As per the Indian government, WhatsApp (530 million users), YouTube (448 million users), Facebook (410 million users), Instagram (210 million users), and Twitter (17.5 million users) reportedly have a collective reach of over 1.61 billion users in India, thereby providing amplified scope for product discovery besides enabling the direct communication on products between buyers and sellers.

Instagram, for example, allows businesses to photo share, do video calls, and host polls, which improves their business planning as they get a pulse on niche or new trends and can develop products to market accordingly. Given that many social commerce businesses tend to have smaller working capital, this flexibility and consumer engagement can be invaluable. Further, the rise of the social media influencer as an established new marketing approach will inevitably strengthen the exposure of social commerce businesses. According to a Bain & Company consultancy report, the social commerce market is currently estimated to be worth around US$1.5 billion to US$2 billion – projected to grow to US$20 billion in five years and US$70 billion by 2030.

Adapting the model, established e-commerce marketplaces are also exploring ways to tap into SME and/or hyperlocal businesses, like Flipkart, which recently launched an independent platform 2GUD to connect offline stores with customers, and showcase products through long-format videos.

Other business models that have spun out of the social commerce space are the reselling and group buying models. Major examples of social reselling platforms are Meesho, GlowRoad, Shop 101, Bulbul, and SimSim – the users of these platforms/apps are called resellers.

The benefits that these platforms include digital inventory of products sourced from suppliers at wholesale prices, logistical services, customer service, integration with social media channels, and even the option of free personal sub-domain and storefront (GlowRoad).

For example, Bengaluru-based Meesho app provides an alternative distribution channel for suppliers to list their wide ranging product catalogs, which can be sourced by individual entrepreneurs by leveraging their contacts on social media. According to the company, as reported by YourStory, Meesho has “built a network of two million ‘social sellers’, nearly 80 percent of which are women… selling goods from over 15,000 suppliers in over 700 small towns. Its app is available in seven local languages, with 40 percent of its daily active users (DAUs) consisting of the non-English speaking population.” Meesho is also one of the most-funded startups in the sector, counting Facebook, Sequoia Capital, Shunwei Capital, SAIF Partners, Y Combinator, among its investors.

This article was originally published on April 8, 2021 and was last updated on May 4, 2022.